Launching a startup is an adventure that’s not just filled with opportunities but also challenges. As a new business owner, you need to handle many responsibilities, and preparing various business documents is one of them.

That’s why you should be prepared to draft all important legal documents for startups and have ready-to-use templates, where possible.

With the fundamental legal documents for startups in place, you can protect your business and prevent any legal problems from arising in the future.

In this article, we delve into 16 essential legal documents that every startup needs to establish a strong legal foundation that will ensure the success of the company.

But first, let’s understand why having the right legal documents for startups is vital.

Table of Content

- Why Do You Need Legal Documents for Startups?

- 16 Important Legal Documents for Startups

- Business Formation Documents

- Articles of Incorporation

- Articles of Organization

- A Business Plan

- Founders Agreement

- Employment Contract Agreement

- Non-Disclosure agreement (NDA)

- Intellectual Property Assignment Agreement

- Non-Compete Agreements

- Advisor Agreement

- Partnership Agreement

- LLC Operating Agreement

- Buy/Sell Agreement

- Employee Handbook

- Bylaws

- Terms of Service Agreement and Privacy Policy

- FAQs

- Conclusion

Why Do You Need Legal Documents for Startups?

Legal documents are more than just bureaucratic necessities for your startup. They serve two major purposes:

- They provide a record of what was agreed upon

- They create rights for each party, enforceable by law

Say, for instance, a disagreement arises between a startup’s co-founders. We know that conflicts occur only when people disagree, and both parties can’t be right.

Some legal documents for startups can help solve these disputes. The conflicting parties can refer to the legal agreement made when starting the business to remind themselves of what was agreed upon.

Sometimes, if circumstances change, or if something is left out of an agreement, one party may choose to challenge the matter in court.

A court case can be a nightmare for a small business, especially for startups with limited funds. It’s time-consuming, costly, stressful, and distracting.

If your agreement is comprehensive and includes everything that could later be challenged you’ll likely stay out of court.

16 Important Legal Documents for Startups

Which legal documents does your startup need?

Every new business has different needs, but the following are 16 critical legal documents your startup will likely need at some point.

1. Business Formation Documents

One of the first things you need to do as a founder is to register your startup as a formal business entity. A legal business entity authorizes your business to operate in any city or region.

There are various types of business entities, each offering different legal protections, as shown in the image below.

Let’s briefly understand these business entities:

- Sole Proprietorship: This is the simplest business structure you can choose for your startup. It requires no paperwork, with very minimal legal requirements

- Partnership: Like a sole proprietorship, a partnership has minimal legal requirements and is more flexible to run than other entity types.

- Cooperation: More structured than any other business entity. It’s complex to form, with strict reporting rules and operation terms. It also offers the tightest legal protection for your (and other founders’) personal assets.

- Limited Liability Company (LLC): The most common entity for a startup is an LLC. It also offers liability protection, without the complex requirements of running a corporation.

Every business structure requires a different business formation document.

For example, if you’re creating a corporation, you’ll need to file for Articles of Incorporation.

When forming a limited liability company, on the other hand, you’ll have to file Articles of Organization. Some states also require a formal LLC operating agreement, while others don’t.

Let’s discuss these two legal documents below.

2. Articles of Incorporation

One of the primary legal documents for startups, especially corporations, is the articles of incorporation.

Your corporation can only be recognized as a legal entity if you’ve filed for the Articles of Incorporation, also known as Charter.

You will be required to submit the following details concerning your startup in the Articles of Incorporation:

- Your startup’s official business name or a DBA in case you’re starting your company as a sole proprietorship or a partnership.

- Your company’s official physical address. This could be a corporate address and a designated registered agent for correspondence.

- A resident agent in the state you’re filing from.

3. Articles of Organization

This is a legal document that you’ll need to file when you form a limited liability company to officially register your startup with the state.

The Articles of Organization document outlines all important details of a limited liability company, such as the rights, powers, liabilities, and obligations of the members.

While each state has its own requirements, below is some mandatory information that you’ll be required to fill out when filing your LLC’s Article of Organization.

- The name of your startup

- The names of the founders of your startup

- Your business address

- The business purpose of your startup

- The names of managers and directors of your startup, if any

- The effective start date of your startup business

4. A Business Plan

One of the most common mistakes that startups make is failing to create a business plan. Many startup founders don’t take time to plan their finances, understand the market, and create a business plan.

As a result, such businesses may lack direction, experience challenges securing funding, and have a high chance of failing.

On the other hand, a research-backed business plan can help you secure investments, identify market opportunities, attract top talent, and improve your decision-making process.

At the very least, consider making a marketing plan and financial plan outlining ways for your business to adapt depending on various contingencies.

The image below shows some of the things to include in a business plan:

Image via Forbes Advisor

Here are some of the critical elements for your business plan to make it more effective:

- Executive summary: A compelling overview of your company and other important details, such as its mission statement, locations, operations, and leadership.

- Product or service portfolio: A detailed outline of the products and/or services offered.

- Funding strategy: Insights into how you plan to raise capital for the business’s short-term and long-term funding needs.

- Exit strategy: A long-term vision for how you plan to transition your business or close it if needed.

- Marketing strategy: A detailed explanation of how you plan to attract and retain your prospects.

5. Founders Agreement

Let’s say you decide to establish a company or form a business partnership with another individual.

In such cases, you’ll need a legal document that clearly outlines relationships between the different stakeholders in your new business.

This legal document is referred to as the founders’ agreement, or sometimes the shareholder agreement.

It’s one of the most important legal documents for startups, and here’s why:

- It details the rights and obligations of each shareholder

- It explains the relationship between the founders

- It comes in handy in case one of the co-founders decides to exit the company

The founders’ agreement includes the details of the terms and conditions of the purchase and sale of each founder’s shares and how these shares can be exchanged.

In a founders’ agreement, the new business partners are given some shares in your company. They’re then considered among the company’s owners and can therefore make critical decisions for the company if needed.

In the long run, a founders agreement facilitates faster conflict resolutions, as well as a smooth founders relationship.

It’s important to note that while there are templates online (like the one above) that can help you create a founders’ agreement, creating a comprehensive one requires legal expertise.

Seeking expert legal services will ensure that your founders’ agreement is thorough and legally valid.

Here are some of the key components that your founders’ agreement should cover:

- Preferential rights: When issuing new shares, include the preferential treatments, if any, that some founders may enjoy. Ensure that you clearly identify these founders.

- Share distribution: Clarify how the shares will be distributed among the different shareholders.

- Board powers: Outline the power that the board of directors has in regulating the transfer or issuance of shares, or legal issues that may arise.

- Termination and exit: Include a strategy for how to dissolve the company or handle any conflict with the company’s stakeholders.

6. Employment Contract Agreement

This implies that if you want your company to have a culture of honesty and transparency, then you need to set a great example by being transparent and honest with your employees.

A great way of doing this is by creating an employment contract agreement that shows what is expected of the employees and the founders.

Employment contracts, also referred to as employment agreements, are legally binding contracts between employers and employees.

They contain critical information about the employment relationship, such as expected work hours, performance expectations, leaves, benefits, and employment duration.

An employee contract is more than just a legal requirement for starting a business. It can help your new business in several ways:

- It adds an extra layer of protection to your business, such as confidentiality.

- It formalizes the arrangement with your new employees.

- It helps provide clarity by outlining employment terms and conditions.

- It sets expectations for an employee’s performance, behavior, and conduct.

- It can contribute to a positive and professional employee-employer relationship.

Keep in mind that your employment contract does not apply solely to full-time employees. You can also use it when hiring part-time employees or freelancers.

7. Non-Disclosure agreement (NDA)

Another important legal document for startups is the non-disclosure agreement.

It’s a legally binding contract used to protect your startup’s confidential information and ensure that sensitive information is only used for a specific purpose.

This agreement is between two or more parties—usually between founders and employees, or among founders.

Startups use their non-disclosure agreements in various ways. Let’s take payment processes, which are a central aspect of startup operations, as an example.

They involve sensitive details of your organization’s financial transactions, payment software, proprietary methodologies, and even business transactions.

It’s therefore important to add provisions related to payment processes within your NDA to guarantee the confidentiality of important information.

Here are some things that should be protected by an NDA:

- Client lists

- Your company’s trade secrets

- Employment contracts

- Sensitive client information

- Proprietary processes

- Marketing strategies

The moment anyone signs a non-disclosure agreement, they’re prohibited from sharing any confidential information protected by the contract with a non-authorized party.

There are three main types of non-disclosure agreements, depending on what you want to achieve:

- Unilateral non-disclosure agreement: An agreement between two parties whereby one party can disclose sensitive information without needing the other party to do the same.

- Bilateral non-disclosure agreement: Both parties agree to hold each other’s confidential information and not share it with any third party.

- Multilateral non-disclosure agreement: Three or more parties decide how they should treat confidential information. At least one party can then disclose the information, while the other parties protect it.

Having a signed nondisclosure agreement document will help protect your ideas and your company’s privacy.

These agreements come in handy, especially when sharing confidential information with third parties like suppliers, independent contractors, and vendors.

Some of the factors you’ll need to specify when preparing your nondisclosure agreement document include the purpose of the confidentiality, the parties involved, exclusions, and breach remedies.

It’s vital to have non-disclosure agreements in place when:

- Sharing confidential marketing strategies, trade secrets, legal documents, and other important details to potential investors, directors, and employees.

- Demonstrating the functionality of new products or services to prospective buyers.

- Onboarding interns or new employees and giving them access to sensitive information.

- Pitching a new business idea or concept to a potential investor or another business owner.

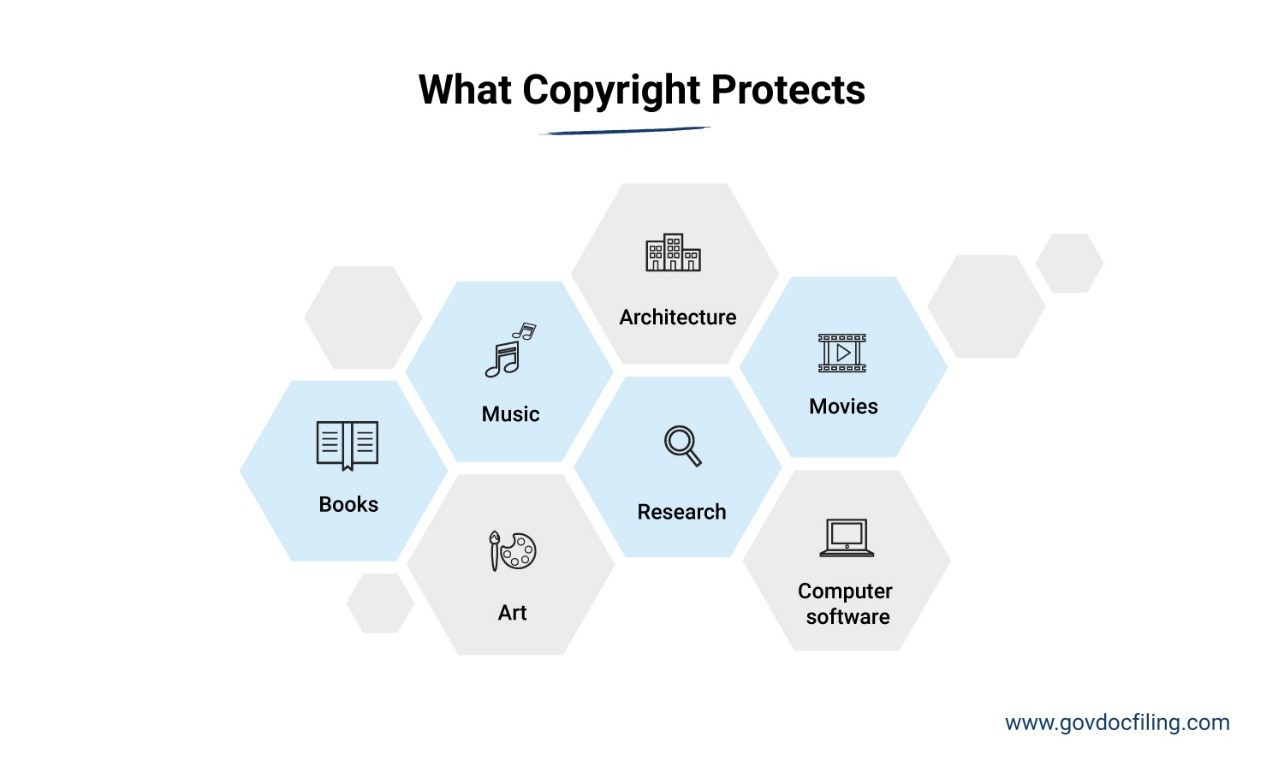

8. Intellectual Property Assignment Agreement

Many startups are built on intellectual property (IP), which is simply anything that can be created with the mind.

This could be a registered intellectual property, such as a pending patent for a new device, or an unregistered intellectual property, such as a software copyright or a trademark.

The image below shows some of the components that an intellectual property like copyright protects:

Without an intellectual property assignment agreement, your company may not truly own the intellectual property.

Let’s say, for instance, one of your co-founders created software before you developed your startup. Without a formal contract transferring the copyright to your company, the individual will own the software even if they co-founded the company.

The same applies to a freelancer who creates intellectual property for you. This may lead to legal issues in case the freelancer refuses to sign the copyright, or if potential investors ask to see the evidence that your company owns the intellectual property.

This is why an intellectual property assignment agreement is considered one of the key legal documents for startups.

Always ensure that your co-founders, employees, and independent contractors sign intellectual property assignment agreements from the outset.

This formal contract will assign intellectual property rights to your business and prevent any challenges in the future.

9. Non-Compete Agreements

Another one of the vital legal documents for startups is the non-compete agreement.

It’s a formal contract that restricts your current or former employees from working for or promoting a competing business for a specified period and within a defined geographical location.

This legal document can also help to prevent talent poaching, which may be a rampant challenge for many startups.

By imposing restrictions on your employee’s abilities to join rival companies or begin competing ventures, these agreements make it more difficult for competitors to recruit your skilled employees.

As a startup founder, it’s crucial to have a non-compete agreement in place to protect the commercial interest of your new business.

Let your employees understand the practical implications of non-competes before agreeing to its terms.

10. Advisor Agreement

An advisor agreement is one of the most vital legal documents for startups, especially if your company seeks guidance, mentorship, and expertise from external advisors.

This agreement formalizes the relationship between your startup and people who offer advice, insights, mentorship, and other forms of support. These could be:

- An independent board member

- A member of your advisory board

- A high-level strategic advisor

An advisor agreement is used when compensation to the advisors is in the form of shares, cash, or a combination of both.

Here are some of the components that you should include in advisor agreements for your startup:

- The scope of an advisor’s services, including the particular areas they’ll be offering their guidance.

- The specific amount or percentage of equity that’s being granted to the advisors.

- Clauses that protect your startup’s sensitive information since advisors may have access to confidential data like trade secrets and proprietary information.

- The specific duration of the advisory relationship and the conditions under which any of the parties can terminate the agreement.

11. Partnership Agreement

It’s often said that starting your business with a partner is a more convenient option as you can share responsibilities and split up the startup cost.

Going this route, however, comes with its drawbacks. For instance, issues may arise from differences between the partners.

It’s even worse if these issues are legally related, as they can drain your business’s resources and you may fail to recover completely.

That’s why a partnership agreement is considered one of the most important legal documents for startups with multiple partners.

Having a partnership agreement in place allows everyone to understand the terms of the partnership and agree to them from the outset.

Below are some issues that, if addressed in your partnership agreement document, will help you define the terms of your partnership:

- The names of the partners

- Duration of the partnership

- Each partner’s contribution to the startup, whether it’s in the form of money, business equipment, or even land

- How new members will be added in the future, if need be

- The next steps to take in case a partner passes on or leaves the partnership

It’s important to note that there are currently no formal requirements to enter a partnership agreement.

Nonetheless, you’ll need to take certain measures to comply with requirements like bookkeeping, tax filing, registration, and regulation.

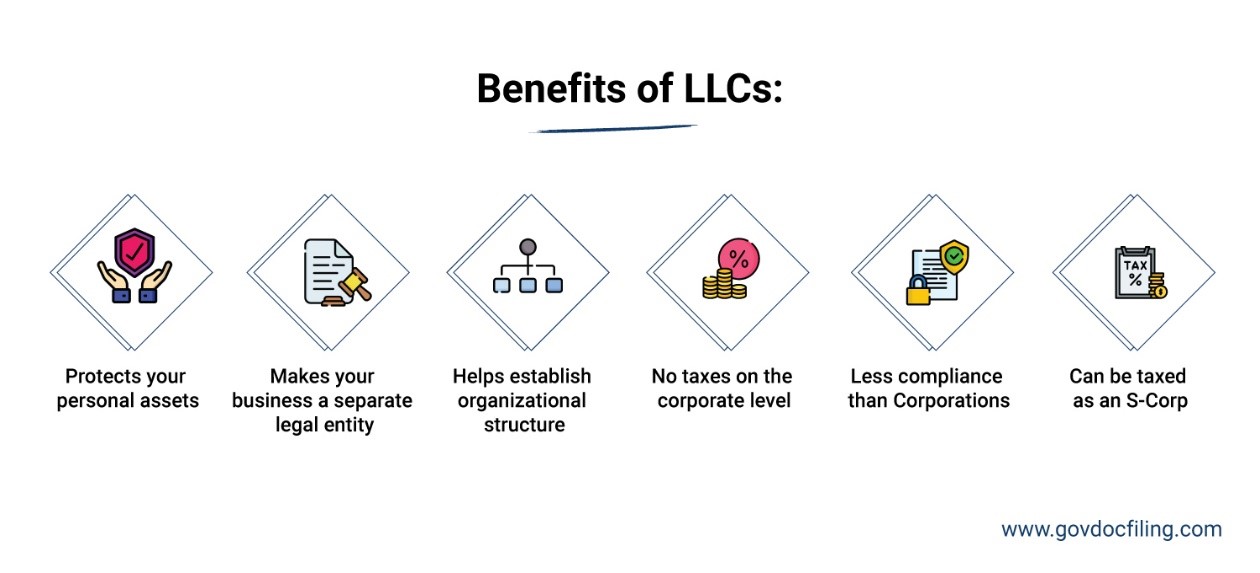

12. LLC Operating Agreement

There are many benefits that you’ll enjoy if you start a limited liability company instead of a partnership or sole proprietorship.

These range from protecting your assets to ensuring great cash flow and making your startup a separate legal entity (see image below).

Image via Gov Doc Filling

With websites like GovDocFiling, it’s become incredibly easy to form an LLC. All you need to do is provide your details and everything will be handled for you.

In case your LLC has two or more founders, you’ll need to create a limited liability company operating agreement. This formal contract will help define how your LLC will function and how it will be taxed.

With an LLC operating agreement, you can set a standard for how you’d like your startup to operate.

The LLC operating agreement is a vital document for your LLC as it mentions:

- The people who own your limited liability company

- How your LLC will be managed and who is/are in charge

- The responsibilities and obligations of every owner

- Whether the LLC should be taxed as an S-corporation or a partnership

Though an LLC operating agreement is not mandated by every state, it’s still recommended that you create one. It will make it easier for you to run your new startup business and avoid potential conflict.

13. Buy/Sell Agreement

Today’s business environment is a highly competitive one, where many startups and small businesses fail or encounter many challenges.

A major factor that has caused many problems for these businesses is the lack of a buy/sell agreement.

A buy/sell agreement is a legal contract that outlines what should happen to a partner’s share if certain triggering events occur.

For example, you or one of the founders may choose to leave the startup or a new member may be brought on board. This agreement will set up these arrangements in advance and make it easier for everyone to transition when the time comes.

Here’s another scenario. As you or your co-founders get older, you’ll want to retire. If you have an heir, you may want to hand over your company on to them.

A buy/sell agreement will come in handy in these situations by helping you determine:

- What happens to your company when any of the above-mentioned situations occur

- Whether the heir will become a partner or they’ll sell their share of the business

Some personal issues may also affect your business. A good example is the case of a divorce or personal bankruptcy.

It can predetermine the business arrangements if these issues arise and protect everyone from the legal hassles involved.

14. Employee Handbook

It doesn’t matter whether a business is big or small; running it without guidelines and policies can be challenging.

A well-written employee handbook helps you communicate the rights and obligations of your company’s staff.

You can also use the employee handbook to lay out the dos and don’ts of your workplace and your expectations.

A great employee handbook should cover topics related to the issues below:

- Workplace harassment

- Standard of conducts

- Employee discipline

- Safety and security

- Equal employment opportunities

- Anti-discrimination

- Employment at-will

15. Bylaws

Bylaws serve as the foundational legal documents for startups, specifically corporations. They are the formal rules and regulations that govern the internal operations and management of the company.

Bylaws are a crucial part of any corporation since they ensure order is maintained while running a company. They also provide clarity on owners’ roles and responsibilities.

Below are the key areas covered by bylaws:

- Voting rights and procedures: Classifies the various voting rights available to different classes of members and establishes how people should vote on each matter.

- Officer roles and duties: Describes the positions of the different officers (director, secretary, treasurer etc.), their responsibilities, and the process of their appointment and removal.

- Financial management: Offer guidelines for financial oversight, including financial reporting, payroll management, and budget approvals.

- Amendments: Create the process for adjusting the bylaws to ensure adaptability even as your startup scales.

- Committees: Detailed explanation of how an organizational committee should be formed in your startup and its purpose.

16. Terms of Service Agreement and Privacy Policy

When launching a startup, particularly one that involves creating a website, the terms of service and privacy policy are essential legal documents you’ll need.

The terms of service agreement, also known as terms of use policy, is a set of rules and regulations that govern how a visitor can use your website or application.

Similarly, a privacy policy informs your site’s or platform’s users how you will use the data and information collected from their site visits.

There are multiple reasons why your online startup needs to have these legal documents:

- You’ll need this to accept payments via your website or app and integrate a payment gateway.

- You can’t take legal action against online users who misbehave on your site, such as hacking or posting abusive content, if you don’t have these agreements.

- By outlining users’ rights and responsibilities, the terms of service document helps to establish clear guidelines for user conduct and permissible activities.

- Your potential clients may not be able to trust you with their information if you don’t have these policies in place.

A well-drafted terms of service agreement can be a great asset to your online business. It includes items like dispute resolution claims, liability limitations, and cancellation clauses.

These components help prevent the misuse of your company’s products and services, offering a sense of safety for both the organization and your customers.

When creating a website for your startup, it’s important to add prominent links to both your terms of service and privacy policy pages.

The links should be easily accessible from any page of your website, placed preferably at the footer section of every page. This will not only demonstrate transparency and your commitment to openness with users but also help save their time and effort.

FAQs

Q1. What are some of the legal issues in starting a new business?

The legal matters you may encounter when forming your business include:

- Choosing a business structure

- Obtaining the right licenses and permits

- Securing financing

- Protecting your intellectual property rights

- Establishing a corporate entity

Q2. Are founders considered employees in a startup?

Founders aren’t really considered employees in the traditional sense. Instead, they’re those who conceive a business idea, take the initiative to start the company, and usually contribute their resources to ensure the startup is up and running.

That said, as a startup scales and grows, there may be a need to hire employees to fill different roles within the company.

In such instances, founders may transition into more formalized leadership roles like executives or managers, and may even receive compensation. They’ll, however, still retain their status as founders or key stakeholders in the startup.

Q3. Who should draft the legal documents for startups?

While it can be tempting to use templates available online or draft legal documents for startups yourself, it’s advisable to seek expert legal services.

A professional attorney should help you draft all your legal documents for startups because of the following reasons:

- An attorney has the necessary experience and expertise to ensure that all the legal documents for startups comply with local, state, and federal laws.

- They can customize your legal documents to meet your company’s particular needs and preferences.

- They’ll ensure that all your important documents comply with the applicable laws and regulations.

Q4. How can I ensure that I have the right legal documents for startups in place?

The following steps will help ensure that you have the right legal documents for startups:

- Register your startup with the right government authorities.

- Consider purchasing insurance such as liability insurance or property insurance, which can help protect your startup from financial loss.

- Establish a clear dispute resolution center where you can handle any legal matters in case they arise.

- Keep accurate records of your financial transactions, employee contracts, and any other legal documents.

- Review and update your legal documents regularly.

Q5. When should startups consider drafting partnership agreements?

Startups need to consider drafting partnership agreements the moment they enter into business partnerships or joint ventures with other entities or individuals.

This can help avoid any legal conflicts in the future since partnership agreements clarify every partner’s rights, obligations, decision-making processes, and mechanisms for dispute resolution.

Conclusion

Starting a new business can be a little overwhelming, but the right legal documents can help you avoid a number of problems that often derail startups.

With the 16 legal documents for startups discussed in this article, you can protect your startup from potential legal matters and ensure its long-term success.

Consider consulting with a legal expert to ensure your legal documents meet all the requirements and adequately protect your interests. All the best!

About the author

From selling flowers door-to-door at hair salons when he was 16 to starting his own auto detailing business, Brett Shapiro has had an entrepreneurial spirit since he was young. After earning a Bachelor of Arts degree in Global and International Studies from the University of California, Santa Barbara, and years traveling the world planning and executing cause marketing events, Brett decided to test out his entrepreneurial chops with his own medical supply distribution company.

During the formation of this business, Brett made a handful of simple, avoidable mistakes due to lack of experience and guidance. It was then that Brett realized there was a real, consistent need for a company to support businesses as they start, build and grow. He set his sights on creating Easy Doc Filing — an honest, transparent and simple resource center that takes care of the mundane, yet critical, formation documentation. Brett continues to lead Easy Doc Filing in developing services and partnerships that support and encourage entrepreneurship across all industries.