Most tax tips get directed to the majority of Americans who go to an office, collect a paycheck, get a W-2, and expect (or at least hope for) a refund at tax time. This post, however, talks about tax tips for contractors and remote workers.

It’s an entrepreneurial age and more and more people work for themselves. Even if they “work” for a big company like Uber or Keller Williams, many of them are independent contractors who document their income for taxes (if they get any documentation at all) on a 1099-MISC.

Remember, as an independent contractor, you are still required to register your business with the IRS. Get your federal EIN here.

Even W-2 employees frequently have a “side hustle” where they get paid on a 1099-MISC. The rules for these kinds of earnings are very different. The one-size-fits-all “W2 refund” tax advice is no longer enough for millions of Americans.

For those who set their own sales, here are tax tips for contractors and remote workers.

Tax Tips For Contractors

The COVID-19 pandemic introduced millions of W-2 employees to the joys of working from home and being independent contractors. This led to an increase in remote work, with people opting for independent contracts over regular employment.

For such independent contractors, self-employment brings with it extra considerations at tax time, often ones for which they need to know a few things.

As mentioned earlier, independent contractors perform tasks as non-employees. Most independent contractors are Sole Proprietors and small business owners.

Those that aren’t running definite businesses are treated as Sole Proprietors by default at tax time.

It’s crucial for employers to distinguish between employees and independent contractors. To determine whether a worker is an independent contractor or not, there are factors that come into play.

These include:

- How much of their work schedule and process you control.

- If their business aspects, i.e. tools and expenses are controlled by the payer.

- The relationship between worker and payer, e.g. Are there employment benefits? Is it a written contract?

If the extent of control to the worker is minimal, they may qualify as independent contractors. Or if their contract simply states so, they’re independent contractors. There are no specific determinants of this relationship, as it’s a combination of factors.

Once it’s ascertained that you’re an independent contractor, you will need to pay your taxes separately from your employer.

You cannot evade paying taxes, but you can maximize your tax savings as an independent contractor by using tax tips. To minimize what goes to the IRS, here are a few tax tips that would help you out.

1. Understand Your Tax Obligation

As an independent contractor, your first tax tip is to understand the nature of your tax obligation. This way, you’ll know exactly what’s required of you and it will help you avoid penalties.

Let’s understand the different types of taxes you may need to pay, as part of our guide on tax tips for independent contractors.

Self-Employment Tax

Independent contractors file self-employment taxes that include reporting their business income and expenses. What is taxed is your earnings or “profit” from your businesses. This means that allowable expenses or deductions can significantly reduce your tax obligation as an independent contractor.

If you’re both employed and have a part-time independent contractor business, you’ll have to file:

- The 1040 form, US Individual Tax Return

- The W-2 Wage and Tax Statement (usually done by your employer)

Independent contractors do not get employment benefits because they’re taxed as both an employer and an employee. As such, you’ll pay your Medicare and Social Security taxes, as an employed person usually would.

In an employment set-up, this is the Social Security and Medicare tax employers withhold from their employee’s pay. You’ll also pay the other half that the employer would normally cover for their employee.

This tax rate is 12.4% for social security and 2.9% for Medicare. To file your self-employment tax, you’ll have to fill the Schedule SE, Form 1040.

Individual independent contractors who earn more than $200,000 in annual income are subject to a further 0.9% Medicare tax.

Income Tax

Find your net earnings by deducting your expenses from your income. If your net earnings are $400 or more, you’ll have to file income tax. However, in some instances, you’d have to file an income tax even if your net earnings are below $400.

All these are federal taxes, and they are filed quarterly. You may also need to pay state taxes, but those vary, depending on where you live.

Taxes Paid By Freelancers

As a freelancer, the IRS treats you as a self-employed Sole Proprietor. Therefore, you have to file self-employment income tax for every client you receive money from. Your clients should issue you a Form 1099-MISC by January 31st of every year.

The form 1099-MISC, or your independent contractor tax form, is a smaller section of the larger form 1040 that reports your self-employment tax.

However, the caveat to the 1099-MISC is that there’s a minimum amount of earnings that are subject to taxation. If a client pays you $600 or more, you’ll receive a form 1099-MISC.

Finding these tax tips for independent contractors useful?

Let’s discuss some more important tax tips that can help you save money and avoid penalties.

2. Switch From Sole Proprietorship To an S-Corporation

As a freelancer, you will file your taxes as a Sole Proprietor, which can be quite high. Our tax tips can help you reduce your taxes. These tax tips are especially beneficial if you earn thousands of dollars.

Change the structure of your small business from a Sole Proprietorship to an S-Corporation, as the latter comes with some extra tax benefits.

What are these tax benefits?

One is that it allows you to protect your personal assets.

The downside to tax filing as a Sole Proprietor is that in case you get sued, your personal assets could be confiscated. This is because a Sole Proprietorship does not protect your personal assets from liability.

In an S-Corp, however, your personal assets will be protected. We know that starting an S-Corporation may be challenging but we can help expedite the process for you.

Also, with an S-Corp, the money you get paid goes to your company and is not considered taxable personal income. What you pay yourself is what gets taxed as income earned. This way, you can pay less in taxes by paying yourself a smaller salary and treating the rest of the money as dividends.

Dividends are not eligible for self-employment income, therefore you’ll end up paying less in taxes, making this one of the best tax tips to save money.

3. Know Your Allowable Business Deductions

Next on our list of tax tips for independent contractors is the importance of learning your allowable tax deductions as a freelancer. This refers to the expenses that the IRS allows you to deduct from your total income as business expenses.

These tax deductions reduce your total taxable income and save you a lot of money when filing your taxes. If you’re having trouble identifying what those are, you can always hire a tax expert, another one of the useful tax tips for contractors.

Many freelancers have trouble with what to deduct and what not.

Some write-offs you can take advantage of include:

- Home office space

- Office supplies

- Hardware and software

- Advertising expenses

- Health insurance

- Internet bills

- Professional service

For Freelancers Working From Home

If you’re a freelance contractor who works from home, this tax tip will be helpful. You can deduct home office expenses, including the rent for the space you use as an office. However, this space must be strictly a workspace and nothing else.

The details of home office spaces are discussed further in this article on tax tips for contractors.

Another advantage of having a home office is the deductible motor expenses. If you leave your house, those miles count as deductibles in your motor expenses.

With an outside office, miles covered commuting to your office are not considered deductible auto expenses.

You can either choose to deduct your auto expenses by mileage rate or actual motor expenses. Keeping your records to make comparisons on which one is more favorable is one of the tax tips that can help you save money when doing your tax filing.

It’s important to note the necessary deductions to your small business to avoid issues during an audit. Personal expenses are not viable write-offs, and this largely depends on the nature of your business. For instance, you can make tax deductions on business calls only, personal calls would not qualify as a deduction.

If you’re finding these tax tips for contractors useful so far, keep reading to find more such useful tips.

4. Report All Your Income

Independent contractor tax is only required to be generated on payments of $600 or more. If you get paid $599.99 or less, no form 1099-MISC is required to be generated. This means that as an independent contractor, some of your income (possibly a great deal of it) might come with no documentation.

You might be tempted not to report this income to achieve some tax savings, but the law requires that you report it. It could become a big problem if you are audited. There are better, safer ways of reducing your tax liability legally.

5. Save All Your Receipts

Many W-2 employees are better off with the standard deduction, an easy one-size-fits-all replacement to listing every allowed deduction.

This is not the case with most independent contractors. Independent contractors can deduct some expenses from their taxable amount, that relate directly to their business.

This makes it a bit complex, as not all these write-offs are straightforward. Mostly, independent contractors have their business and personal lives intertwined, making separating said expenses difficult.

Therefore, one of the useful tax tips for contractors is to save all the receipts to help you keep track of your expenses more accurately.

Earlier on, we went over some summarized versions of these tax deductions. Here are some specifics to shed more light on the receipts you should always have at hand.

- Purchases like phones and computers can be deducted as equipment costs

- Insurance premiums, e.g. medical covers

- Certain meals can be deducted as business expenses

- Certain education or personal development expenses

- Designate a car as a “business lease”

- Advertisements and promotions

- Legal and professional fees, e.g bookkeeping, tax advise

- Internet and phone bills

- Write off the entire cost of a heavy vehicle like an SUV as a “fleet vehicle”

These tax deductions really add up. They could even make the difference between big tax savings and tax credits. If called on to prove these expenses, you will need receipts.

Get receipts by email or text if possible so you don’t have to dig through balled-up scraps of paper.

6. Pay Your Taxes Quarterly

One of the important tax tips for contractors and remote workers is to pay taxes quarterly every tax year.

Most employees get a refund come tax season because employers perform tax withholdings and deposit those withholdings monthly. Those withholdings are conservative. The goal is to get the tax base to pay more than they ultimately owe so that the government can issue a slew of refunds, rather than having to collect money due at the end of the year.

None of this applies to independent contractors. As tempting as it is to pocket every dime, independent contractors are required to make quarterly deposits of estimated taxes.

This includes allotments for Social Security and Medicare included in the Self-Employment (SE) tax, and income taxes on the profits of your business, as mentioned earlier.

Filing taxes quarterly will help you reduce your tax obligation by the end of the year and keep you from being penalized. Here’s how to estimate your quarterly tax obligation.

Use form 1040 to help determine your estimated tax payments for the year. Take this estimated amount and divide it by four to get your estimated quarterly taxes.

Another effective and perhaps the best way to keep tabs on your quarterly taxes is through bookkeeping. Using accounting software will help you keep track of all your income and expenses, giving you a more accurate tax estimate.

If there are any significant financial changes along the way, that affect your taxes, then make the required adjustments.

To avoid tax penalties, file your quarterly tax income before the set deadlines. Here are the 2022 deadlines.

| Period | Deadline |

| 1st Quarter | April 18th, 2022 |

| 2nd Quarter | June 15th, 2022 |

| 3rd Quarter | September 15th, 2022 |

| 4th Quarter | January 17th, 2023 |

When you eventually file your annual taxes, you’ll only pay the balance that the quarterly payments did not cover. Also, if you have an overpayment on your 1040 Form, the IRS will issue a tax refund when you file an income tax return form.

However, you can apply to have the overpayment or part of it be taken to next year’s estimated tax payments, rather than have it refunded.

You can then use your accurate income tax for the year to estimate your next year’s quarterly estimated tax payments.

7. Find Out If You Can File a Schedule C-EZ

1099 tax is filed on a tax form called Schedule C. However, you should check if you have the option to instead file on Schedule C-EZ. A schedule C-EZ, unlike Schedule C, is much easier to fill out and will save you lots of time.

Here’s why.

Instead of filling out your business expenses by category like you would on Schedule C, you lump them up together. So the trouble of having to determine whether an expense is a rent expense or an advertising expense, e.t.c., goes away.

Independent contractors qualify to use Schedule C-EZ instead of Schedule C if all the following apply.

- $5,000 in business expenses or less.

- No inventory at any time of the year.

- Cash method of accounting.

- No employees were hired ever throughout the year.

- No depreciation of business property.

- No tax deductions for business use of your home (more on that below.

- No passive activity losses carried over from the previous year.

Please note that, if you do not meet any of the above qualifications, you may not use Schedule C-EZ.

Consult a professional if you need help to determine if any of this applies to you. Also, this is an evaluation you ought to make annually. The qualification to use Schedule-C-EZ in a single year doesn’t make it so for future periods.

Now that we’ve covered the most important tax tips for contractors, let’s discuss the tax tips for remote workers separately, in the next section.

Tax Savings Tips If You Work From Home

With the pandemic came new working dynamics, and so many people switched to remote work. Working remotely comes with its perks. Besides the flexibility and convenience, there are tax advantages people working from home can take advantage of. This is especially so for self-employed remote workers. The major tax advantage for remote workers is the deductions available to them.

If you’re an employee and still run your gigs on the side, you’re self-employed part-time. Therefore, these home tax deductions apply to you too, to an extent.

As long as you do not work your W-2 job on this said space, the IRS allows you to apply the deductions. For instance, you can have separate spaces for your employment work and your independent side gigs.

Here’s a deeper look into some of the tax tips remote workers can use to save money.

8. Consider a “Home Office” Deduction

Do you have a spare bedroom dedicated to an office? A corner of the living room? A corner of the garage? Are you also a self-employed remote worker?

Even if you’re freelance or are an independent contractor part-time, the IRS allows you, as long as you work from home, to write off a portion of your housing expense as a “home office” expense. This is one of the lesser-known tax tips that can save you lots of money.

Provided that part of the home is devoted solely to work, it will qualify for the deduction. Here are indications that your space qualifies as a home office.

- You conduct most of your business in your home office.

- It’s your fixed administrative location and there’s no other. You conduct administrative work, or management work in your home office regularly.

- You meet your customers at home

- This space is where you store your inventory

- You run a daycare center from home

- You use a separate structure in your home for business e.g your garage

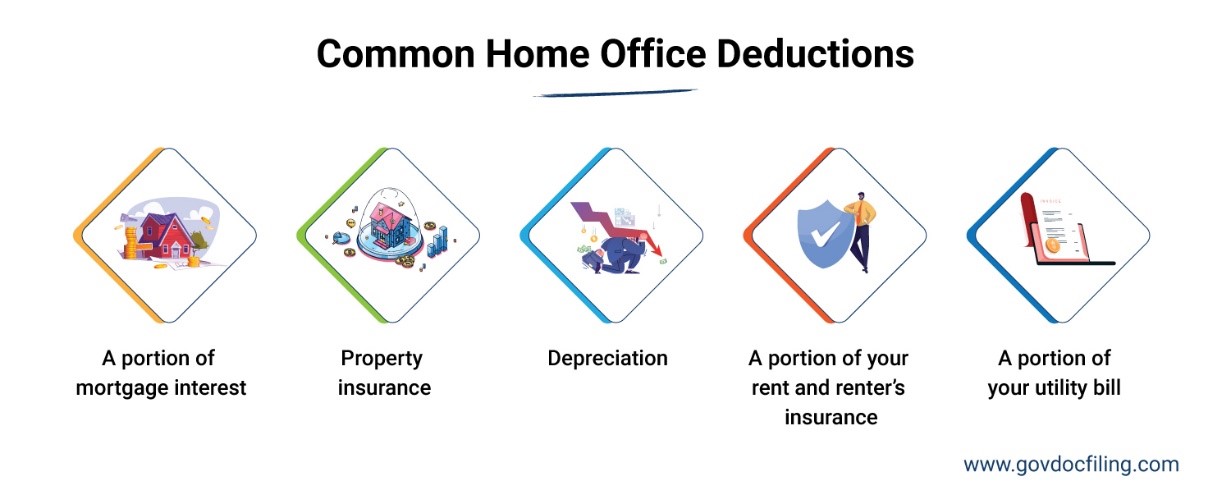

Home office deductions could encompass:

- A portion of your mortgage interest

- Property insurance

- Depreciation

- A portion of your rent and renter’s insurance

- A portion of your utility bill.

Using Form 8829, you can figure out the allowable expenses of using part of your home for business.

When making your home office deductions, you can either use the simplified or the regular method.

9. Switch Between Simplified and Direct Method As Needed

With either method of home office deduction, you’re likely to get different values. This tip can help you, as an independent contractor, to take advantage of the method that gives you a higher deduction. This is one of the tax tips that can help you save money on taxes.

Before you decide which method saves you more money, let’s understand how each works.

Simplified method

This method was introduced in 2013 by the IRS to simplify taxpaying for remote workers and that’s why we’ve included it in our list of top tax tips.

With the simplified method, you can add tax deductions of $5 per square foot of your home office. This deduction, however, has a cap of $1500 per year, making it only suitable for smaller offices of up to 300 square feet.

The advantage of this method, as the name suggests, is that it’s simple. You don’t need to keep a record of your home expenses, such as your mortgage, your rent expense, or your office space utility bills. Also, you will not need to split these deductions between your personal and work use.

If you’re a homeowner and you’re using this option, you cannot claim a depreciation deduction. This also means you will not need to account for depreciation, a calculation that could get confusing.

This method is appropriate for smaller spaces. Most homeowners can get higher deductions than $1500 annually on their taxes. If this is the case with you, you may consider the direct method.

Direct Method

The direct method is a little more complex and requires you to keep all your records intact. These include all your home office expenses and other repair costs and utilities. It also includes indirect expenses that relate to your entire home.

The expenses that directly relate to your office space are easy deductibles, as you can deduct them in full. These include repair and maintenance, e.g. painting your home office.

The expenses relating to your entire home are only partially deductible. However, they have to directly serve your home office. For instance, expenses such as repairing a furnace can be partially deducted as the furnace also heats your office. While repairs to improve your home’s look may not qualify as a deductible office expense.

One way to determine this partial expense is by figuring out what percentage of your home the office space occupies in square feet. Take this percentage and multiply it by all your total house expenses and you have your deductibles.

One of the most useful tax tips is to calculate your tax deductions using both methods, every year, and choose the most beneficial one. This is one of the most useful tax tips to save money.

10. Consider Deducting Other “Work-Related” Household Expenses

Your “home office” isn’t the end of the deductions available to employees. You might consider writing off expenses with a work application, even if they also have a household application.

Obvious examples include an internet bill, cell phone bill, landline bill, or Amazon Prime delivery bill. The fact that you use these services for non-work purposes does not necessarily void them as a deduction as you can use them for business.

Other deductions are explicitly business-related expenses even though they do not relate to your home. For instance, making business cards, business lunches, hiring help to create your business logo e.t.c.

Check the rules carefully, and seek professional tax advice if you are not sure what you are allowed to deduct.

11. Be Aware of Deduction Limitations

Employee expenses are reported on Form 2106, Line 21 of your Schedule A: Itemized Deductions. Some limitations to keep in mind when selecting expenses to deduct include the following:

- Remember, the standard deduction still results in more tax savings, even if you work from home. If you choose the standard deduction instead of itemized deductions, you cannot deduct your home office or other expenses. The standard deduction takes the place of itemized deductions.

- Employee expenses are considered “miscellaneous deductions,” which cannot exceed 2% of your income.

FAQs

1. What is the tax on self-employment income?

Self-employment tax is paid by independent contractors, freelancers, Sole Proprietorships, Partnerships, Single Person Limited Liability Companies, or S-Corporations.

It’s a 15.3% tax rate that includes 2.9% Medicare tax and 12.4% Social Security tax. It applies to your net earnings, i.e after you deduct your business expenses from your income.

One of the tax tips to reduce your self-employment tax is switching from a Sole Proprietorship to an S-Corporations as it provides more tax benefits.

2. How do I calculate my self-employment tax?

The amount of your net earnings that is subject to self-employment tax is 92.35%. You calculate your net earnings by taking your total income and deducting your business expenses.

These include home office expenses if you work from home. If your earnings are over $400, then you’ll be subject to the 15.3% self-employment tax.

3. How can I lower my self-employment tax?

You can utilize these tax tips to lower your self-employment tax:

- You can take advantage of the business expense deductions available to you. This in turn reduces your net earnings and you pay less tax.

- Switch from Sole Proprietorship to an S-Corporation. This is advisable if your earnings are high. Switching to an S-Corporation lets you take advantage of its independent entity status. Therefore protecting your personal assets from liability.

Also, the income you receive doesn’t come directly to you, but to your corporation. You can then only pay tax on the salary you pay yourself.

Use these tax tips for contractors and remote workers to get tons of tax savings.

4. What is a direct expense for a home office?

Direct expenses for a home office relate to the specific office space and the items in it. These include the cost to maintain the space, depreciation of furniture, improvement costs, and repair costs.

5. How is the home office deduction calculated?

To calculate your home office deductions, you can use two methods:

- Simplified method: It’s appropriate for small size offices. Here, you calculate your tax deduction by square feet. You can only deduct $5 per square foot. The cap on this is $1500 annually.

- Regular method: This includes the direct expenses relating specifically to your office space and other indirect expenses. The indirect expenses are for the entire house and when calculating them, you do it partially. You take the percentage of the house that your office occupies and use that to multiply by the expenses of your house that directly affect your business.

One of the tax tips for contractors who work from home is to calculate the deductions using both methods and choose the most beneficial option each year.

6. What depreciation method is used for a home office?

You can only deduct depreciation expenses if you own your home. To do so, depreciate your property annually on a straight-line basis over a period of 39 years. This is the provision by the IRS for homeowners.

7. What income can be excluded from self-employment tax?

Independent contractors or small businesses with earnings of less than $400 are not subject to self-employment income.

Other than this, there are several tax deductions mentioned in this post on tax tips for contractors that you can make to reduce your taxes.

8. What can you write off as an independent contractor?

Here are a few tax deductions you may claim as an independent contractor:

- Home office expenses

- Health insurance

- Educational expenses

- Vehicle expenses

- Phone and internet bills

- Business meals

Use our tax tips for contractors to save money on taxes and avoid penalties.

9. Do self-employed people get a tax refund?

Just like regular employees, self-employed people can have tax refunds too if they file the 1040 form. This is because they pay estimated taxes every quarter and not the accurate tax for the tax year. This way, they may end up paying more in income taxes than they owe. In such instances, they can get a tax refund.

Ready to Use These Tax Tips for Contractors?

Understanding the tax implications of your business model just about summarizes all the above tax tips for contractors and remote workers. Whether you’re a 1099 contractor or you’re running a Sole Proprietorship or even a single-person LLC.

Knowing your business model first helps you distinguish your personal income and expenses from your business transactions. With that, you can easily understand your tax obligations and save money in the process using our tax-saving tips for contractors.

While some of these tax tips may seem straightforward, it is always a good idea to work with a business tax professional like bench.co to help manage your books throughout the year.

If you have not yet completed your business formation and are unsure which business entity is right for you, take this simple survey. Our simplified, one-page form can help you set up your business at both the state and federal levels. Click here to get started.