Most companies elect S-Corp status to avoid the double taxation that C-Corporations get subjected to. However, this does not mean that S-Corps do not get taxed twice entirely.

So how are S-Corp distributions taxed?

This post takes you through everything you need to know about S-Corp income distributions, non-taxable dividends, taxable distributions, and much more. By the end, you’ll be able to know which forms your S-Corp entity and shareholders need to fill out for different tax obligations.

Distribution of taxes on S-Corporations depends on a few things at both the shareholder and corporate levels. These include:

- Shareholder’s basis on corporate stock

- S-Corp earnings and profit (E&P)

- Accumulated adjustment account (AAA)

These are all discussed in detail in the next sections. But first, here’s an overview of what an S-Corp is and why they’re taxed differently from C-Corporations.

What is an S-Corporation?

When a company does an S election, all the income, and credit loss deductions pass through to shareholder’s personal earnings and are taxed as such. Companies choose to be S-Corps to:

- Avoid double taxation

- Have company losses pass through to shareholders

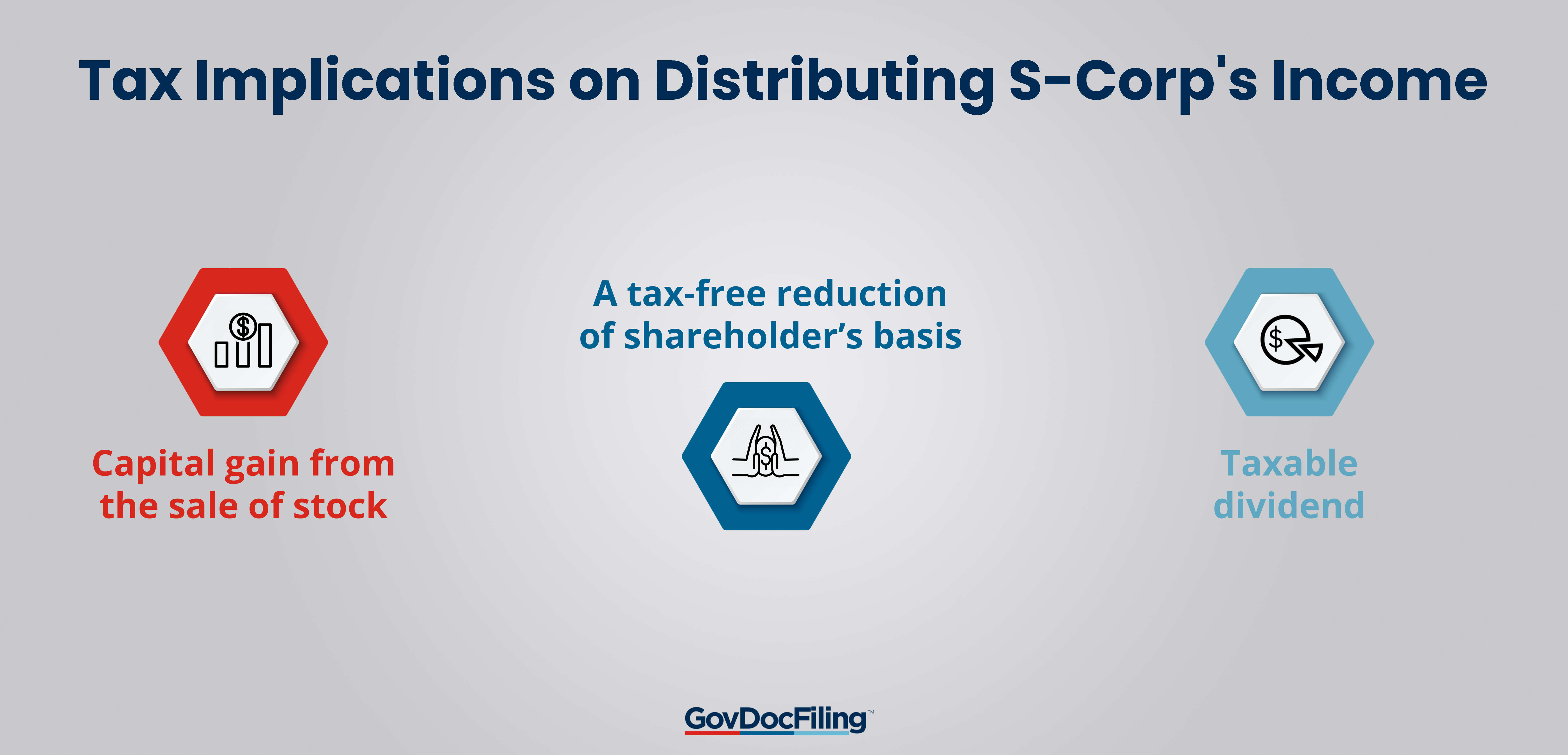

An S-Corporation’s distribution of income and property can lead to three tax implications for the shareholder. These include:

- A tax-free reduction of shareholder’s basis

- Capital gain from the sale of stock

- Taxable dividend

These implications are not mutually exclusive and income and property distribution can lead to more than one outcome.

(You can elect to become an S-Corp now through Inc Authority or Incfile.)

Why S-Corps are Treated Differently From C-Corps

Before discussing in detail how S-Corp distributions are taxed, it’s important to note how they’re different from C-Corporations.

C-Corporations are guided by Subchapter C, which requires entities to be taxed both at the corporate and shareholder level. A C-Corp is taxed when it earns income as well as when the income is distributed to shareholders as dividends.

S-Corps are generally subject to single taxation. This means that Income earned is not taxed at the entity level, but is distributed amongst shareholders who then report these dividends on their individual tax returns.

All these differences are preserved under Section 1368 by the IRS.

How are S-Corp Distributions Taxed?

As mentioned earlier, S-Corp distributions are taxed based on corporate-level attributes (AAA and E&P) as well as shareholder-level attributes (shareholder tax basis).

Here’s an in-depth review of these key attributes for determining S-Corp distributions:

Shareholder’s Stock Basis

According to Section 1367 of the IRS laws, an S-Corp shareholder needs to adjust the value of the stock they own every year to represent any income gain, loss, deduction, and distribution items that apply to that shareholder.

S-Corporations are only taxed at one level, so these yearly changes are needed to keep it that way. These adjustments can lead to either an increase or decrease in a shareholder’s stock basis.

A shareholder is required to increase the basis of their S company stock for:

- Capital contributions

- Both taxable and tax-free income

- The amount by which depreciation deductions exceed the property’s basis

Additionally, a shareholder is also required to reduce their stock basis for distributions that aren’t taxed as dividends under Section 1368. These include:

- Any loss and deduction (including non-deductible expenses that shouldn’t be charged to a capital account).

- The amount of a shareholder’s depletion deduction, as long as it doesn’t exceed their share of the adjusted basis of any oil and gas property held by the S-Corporation.

The order in which these changes need to be made is the most important thing. This is because distributions lower the stock’s basis. But in many cases, the stock’s basis is what determines whether or not a payment is taxed.

The general rule of thumb is to increase the necessary stock basis first, then subtract any distributions before losses. You can then deduct any costs that aren’t tax deductible and finally any other loss or deduction.

The stock basis cannot fall below zero.

Let’s suppose losses exceed the remaining stock basis after distributions and non-deductible costs are subtracted. In that case, the excess losses can be used to reduce the shareholder’s basis in any debt owed by the S-Corporation to the shareholder.

So long as the losses don’t go over the shareholder’s stock and debt basis, they are suspended and can be carried forward forever.

When an S-Corporation has no accumulated E&P at the time of a distribution, a shareholder’s stock basis will be the only thing that matters in figuring out if the dividend is taxable.

Here’s more on earnings and profit.

You May Also Like:

Earnings and Profit (E&P)

An S-Corporation can have E&P in one of two ways:

- If the Corporation had E&P from its years as a C-Corporation before acquiring its S-Corp status.

- If an S-Corporation bought almost all the assets of a C-Corporation in a transaction done as per Section 381. According to this section, the S-Corporation has to take over the E&P of the entity acquired.

When an S company that was previously a C Company makes a distribution with accumulated earnings and profits (E&P), it becomes harder to determine if the distribution for the year is taxable.

Usually, this additional layer of complexity is needed to maintain the second level of taxation for C-Corps which must happen when income is distributed to shareholders.

This is because in such cases, an entity’s E&P balance is the item that determines the amount of distribution that is taxed twice.

By choosing S status, a Corporation can’t get out of paying taxes twice under Subchapter C — at least for any earnings and profit accumulated before the S-election takes effect.

The accumulated E&P will be taxed as a dividend when distributed, even though the entity has become an S-Corporation.

(You can elect to become an S-Corp now through Inc Authority or Incfile.)

Accumulated Adjustment Account (AAA)

As stated above, any accumulated E&P at the time of an S election still gets taxed as dividends to the recipient shareholders when distributed.

Even though this is the case, the law is set up so that an S-Corporation can distribute the income earned before it is treated as having made a distribution from E&P. This causes a delay in the effect of a taxable dividend and it only applies to an S-Corporation’s AAA.

So what’s an accumulated adjustment account?

An S-Corp’s AAA is the account that is used to track the total taxable income that has not yet been distributed to shareholders.

This means that a newly elected S-Corporation will always start with a zero balance in its AAA, even if it has E&P or retained earnings from its previous years as a C-Corporation.

The more money there is in the AAA account, the less likely it is that a payout will be taxed as a dividend. Therefore, when an S-Corporation has accumulated E&P, it’s important to maintain an AAA.

An AAA separates distributions made from the C-Corporation’s E&P, which must be taxed as a dividend to shareholders, from S-Corporation income, which isn’t subject to double taxation.

What’s more?

An S-Corporation must change its AAA every year in the same way that shareholders must change their stock basis. However, unlike shareholder stock basis, the AAA is an entity-level item that is not affected by any shareholder transactions.

When adjusting your AAA, your amounts increase for the same reasons as those of your shareholder stock basis, except:

- Capital payments

- Income that isn’t taxed

Similarly, it decreases for the same reasons except for those expenses that are tied to tax-exempt income and can’t be deducted.

Contrary to the shareholder stock basis, AAA amounts can go below zero, but only because of losses and not because of distributions.

Like the required changes to stock basis, the order in which you make the yearly adjustments is the most critical part of maintaining the AAA.

Here are the steps to follow:

- First, the S-Corporation must figure out if its net adjustment for the tax year is positive or negative.

- A net negative adjustment is an amount by which the AAA balance went down more than it went up during the year if you exclude distributions.

If an S-Corporation has a net negative adjustment for the year, AAA is decreased by the distribution, but not below zero, before it is reduced by the net negative adjustment. This raises the AAA balance and makes it less likely that the payment will be a taxable dividend from E&P.

- Though not a regulation, it’s helpful to think of a “net positive” adjustment as and when gains to the AAA outweigh other cuts that aren’t distributions.

If an S-Corporation has a net positive change for the year, that adjustment is made to AAA before any distributions made for the year are subtracted from AAA.

This rule is good for shareholders because it keeps the balance of the AAA high, making it more likely that a payment will be counted as coming from the AAA and not from dividend-paying E&P.

It’s important to note that the AAA is still different from the shareholder’s stock basis, even when a company is fully owned by a single shareholder.

Treating AAA and stock basis as the same only makes it harder for you to determine if distributions from an S-Corp are taxable and, in most cases, you’ll end up with incorrect figures.

You May Also Like:

General Taxable S-Corp Distributions at a Glance

Distributions made by an S-Corporation with accumulated E&P are treated differently under the regulations than distributions made by an S-Corporation without accumulated E&P.

Distributions from an S-Corporation are taxable only if the S-Corporation has accumulated E&P in the year of distribution, therefore this must be established first.

As discussed earlier, cumulative E&P is only available to an S-Corporation if it has either been a C-Corporation in the past or has purchased the assets of a C-Corporation in a Section 381 transaction.

If an S-Corporation has always been an S-Corporation and has never purchased the assets of a C-Corporation in a Section 381 transaction, then the S-Corporation cannot have E&P.

It’s crucial to ascertain whether or not E&P has been accumulated by your S-Corporation.

The taxability of a distribution made by an S-Corporation is simple to find out if the company has no accrued E&P. The opposite is true if the S company has accrued E&P at the time of the distribution, making it more difficult to determine whether or not the distribution is taxable.

(You can elect to become an S-Corp now through Inc Authority or Incfile.)

Taxable S-Corp Distributions for Entities Without Accumulated E&P

When an S-Corporation with no accumulated E&P makes a distribution, the payment is taxed in two ways:

- First, the shareholder’s basis in the Corporation’s stock will be reduced by tax-free distributions.

- Second, any distribution that is more than the shareholder’s stock basis is viewed as capital gain from the sale or exchange of the stock in question.

There’s no mention of the S-Corporation’s AAA balance in these rules, which is a big deal. If there’s no accumulated E&P, there’s no need for an AAA because a payout cannot be a taxable dividend made from E&P.

So, the AAA balance has nothing to do with whether or not distributions from an S-Corporation with no accumulated E&P are taxable. The only thing that matters is the shareholder’s basis in the company’s stock.

Taxable S-Corp Distributions for Entities with Accumulated E&P

Any earnings and profits (E&P) distributed by an S-Corporation must be tracked down to their source.

As mentioned earlier, this is done to ensure that shareholders of S-Corporations aren’t double-taxed on earnings and profits (E&P) distributed to them, as is the case with shareholders of C-Corporations.

To achieve this goal, Section 1368(c) categorizes distributions from an S-Corporation with accumulated E&P into three categories for purposes of calculating the tax liability of the recipient shareholders:

- One, if the AAA has a positive balance, the distribution is accounted for as if it were made by a S-Corporation with no accumulated E&P to that extent.

- Second, dividends are paid out to the extent of the accumulated E&P balance for distributions above the AAA threshold.

- Lastly, distributions made by an S-Corporation with no accumulated E&P are deemed to have been made by the Corporation.

The regulations allow a Corporation to distribute its remaining undistributed after-tax income before the Corporation is deemed to have distributed its accumulated E&P.

This is accomplished by treating the first distribution amounts as having been made from an S-Corporation with no E&P to the extent of the AAA balance.

However, this only means that the distribution will neither be treated as a taxable dividend nor as income for the recipient. The shareholder’s basis in the Corporation’s stock must be adjusted to calculate the taxable amount of the distribution.

Any amount of the distribution over the shareholder’s stock basis will be considered a capital gain, and the shareholder’s stock basis will be reduced by the amount of the distribution.

The regulations state that once an S-Corporation’s AAA is zero due to a distribution, any further distributions will be made from the Corporation’s accumulated E&P and will be taxed as a dividend to the recipient shareholders until the E&P balance is reduced to zero.

Once a Corporation has distributed all of its accumulated E&P, it can no longer pay taxable dividends.

From there on, the basis of the shareholder in the Corporation’s stock will be the only determinant of whether or not the distribution is taxable. And as already mentioned, if the distribution exceeds the shareholder’s basis, the excess will be treated as capital gain rather than a taxable distribution.

In summary, the taxable status of a distribution from an S-Corporation that has accumulated E&P is determined by adjusting three distinct attributes:

- The S-Corporation’s accumulated after-tax additions (AAA)

- The E&P

- The shareholders’ stock basis

(You can elect to become an S-Corp now through Inc Authority or Incfile.)

Property Distributions

An S-Corporation must account for property gains if it sells the appreciated property to its shareholders at its fair market value. The fair market value must be greater than any liabilities attached to the property that the recipient of the distribution agrees to take on.

Then, the basis of each shareholder’s stock in the company must be increased by the amount of the shareholder’s proportionate share of the gain.

Once the liabilities are subtracted from the property’s fair market value, the S-Corporation is considered to have made a distribution to the shareholder.

The S-Corporation cannot take a loss if the fair market value of the distributed property is less than its adjusted tax basis.

To avoid double taxation, the S-Corporation could sell the property to a third party and use the proceeds to pay down debt or reward shareholders.

You May Also Like:

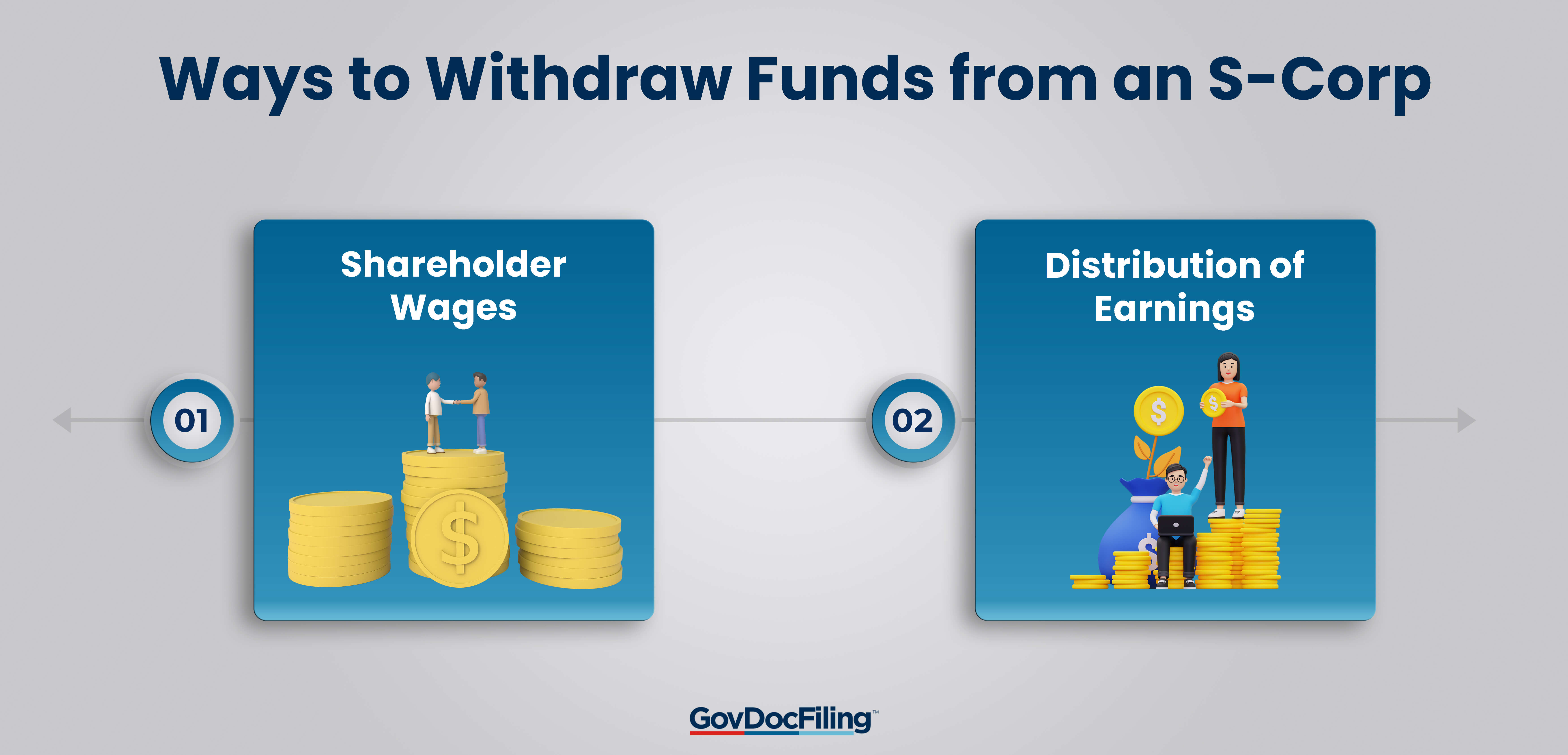

Withdrawing Funds from an S-Corporation

S-Corporation owners have options for getting money from the business. These include:

Shareholder Wages

Every shareholder who works for an S-Corporation is considered an employee. This means that, for tax purposes, they’ll be treated like non-shareholder employees. They’ll receive a paycheck with a W-2 form, that’s subject to withholding tax and employment taxes. You can use Gusto or ADP to process the paychecks.

Distribution of Earnings from an S-Corporation

The distribution of earnings from retained earnings by a regular C-Corporation is deemed a dividend. Shareholders of a C-Corporation need to fill out Form 1099-DIV and disclose their dividends on their individual federal tax returns.

S-Corporations make tax-free non-dividend distributions unless the distribution exceeds the shareholder’s stock basis. In such cases, the excess distribution amount is taxed as a long-term capital gain. Social Security and Medicare taxes do not apply to distributions made by an S-Corporation.

FAQs

Q1. Are dividend distributions from S-Corp taxable

A. Dividend distributions in S-Corps are generally non-taxable. This, however, does not absolve shareholders from paying taxes on profits the Corporation makes. For instance, the profits that an investor receives as a shareholder are subject to taxation.

Q2. Are S-Corp distributions considered income?

A. S-Corporation distributions are earnings made by the entity which are passed through as dividends to owners and taxed only at the shareholder level. The amount of taxable distribution depends on a shareholder’s tax basis, a business’s E&P, if any, and their AAA.

Q3. How do I pay myself distributions from S-Corp?

A. In an S-Corp, owners have two options to pay themselves. The first is shareholder wages or salary, which the IRS considers taxable income. The other is through the distribution of earnings, which are generally not taxable if the S-Corp does not have any earnings and profit.

Q4. Where do distributions from S-Corp go on tax returns?

A. Distributions are considered taxable when a company has earnings and profit or when the amount of distribution exceeds a shareholder’s stock basis. The former is a taxable dividend reported on Form 1099 DIV while the latter is treated as a long-term capital gain reported on Schedule K-1.

Q5. Are S-Corp distributions included in adjusted gross income?

A. Yes. Unlike C-Corporations, if your business is an S-Corporation, your adjusted gross income (AGI) will include your net gain or loss from your Corporation. C-Corps file their tax returns at the corporate level, so the income is not included in your AGI.

S-Corp Taxable Distributions: Summary

Generally, S-Corps have the upper hand over C-Corps in taxation since they’re not subject to double taxation. However, as discussed, in more nuanced situations, S-Corp distributions are taxed depending on various other factors.

This is especially so if your S-Corp was previously a C-Corp.

At the shareholder level, the item to consider is a shareholder’s stock basis in the Corporation. Similarly, at the corporate level, the items in consideration include the entity’s earnings and profit as well as its accumulated adjustment account.

Otherwise, companies with no E&P have fewer complications determining how their distributions are taxed.